Atos Buys Bull To Commercialize HPC, Build Out Cloud

Atos, the European IT services giant based in France that is the amalgam of a dozen companies that have been brought together over the past several decades, is getting into the systems business through the acquisition of French IT supplier and services supplier Bull.

It is interesting to contemplate if similar deals will follow.

Bull has a long and complex history, like Atos, and is well regarded for the engineering of its systems, particularly in recent years in the supercomputing space. Thierry Breton, who is chief executive officer at Atos, a former CEO at Bull in the 1990s, and a former minister of finance for the French government, is attempting to create an IT giant that can span Europe as well as dominate its home market. The combined company will not just be a managed services and outsourcing giant, but will leverage the deep infrastructure and system software skills of Bull to create a unified stack from the hardware out to application software to help companies design products and process massive amounts of data.

Cloud computing and big data are fast-growing areas that Breton called out as important propellants of the deal, which will see Atos pay €4.90 per share in cash or about €620 million ($844 million at current exchange rates between the dollar and the euro) for Bull, which had €1.26 billion ($1.72 billion) in revenues in 2013. That is about a 30 percent premium over Bull's average share price in the three months prior to the announcement of the deal. The fact that the price is about half of a year of Bull's revenues shows just how tough it is in the IT infrastructure and services market these days.

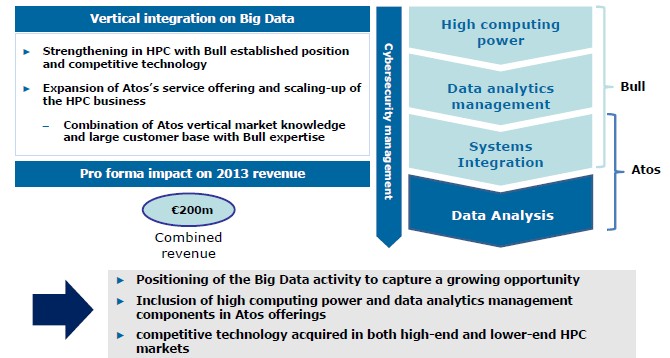

On a call with analysts and journalists to go over the proposed acquisition on Monday, which was a the Memorial Day holiday in the United States, Charles Dehelly, senior executive vice president of global operations at Atos, spent a lot of time talking about the synergies between Bull's systems and Atos' software and services expertise and how this would be leveraged in the big data and cloud markets, which are growing faster than other parts of the IT sector where the two companies play right now.

Bull currently has a 16 percent share of the €900 million market for HPC systems in Europe, according to Dehelly. Bull can build and support petascale systems and has also reached down lower with a new line of smaller machines. But Atos wants more than to control its own supercomputing business. It wants to leverage that to chase the data analytics opportunity, and equally importantly, make its own systems to sell to customers and to use in its clouds.

"Our clients are digitalizing their businesses and the strategic value of their data has been growing at an accelerated pace," explained Dehelly on the call. "Four our clients, to be able to capture the value in their data, they have to master the whole value chain, from the product layer on top of which their data is analyzed, to the infrastructure software and the applications that process that data to the algorithms that the data scientists create to extract insight an opportunity. Clients do not seek hardware and statistical tools, but they look for solutions that integrate all of their needs and bring together those assets in an efficient way."

These are recurring themes here at EnterpriseTech: leveraging advanced technologies for competitive advantage in the enterprise and providing a finished stack that performs a set of tasks. (Can we all find another word for solution? As we all know, any solution is just a temporary solution because it needs to be altered to match changing conditions.)

The way the pieces come together, Bull will be supplying the high performance infrastructure and software for optimizing the systems and dataflows, while Atos has the system integration and data analysis skills. Atos, which manages communications networks for some of the largest banks in the world, is also supplying security for the whole shebang:

The combined HPC and big data businesses at Atos and Bull accounted for €200 million in sales in 2013, and the plan is to scale up the traditional as well as enterprise HPC business. Atos reckons this business is growing at double digit rates and while much smaller than other parts of the company, it is important and, significantly, able to generate profits with a solution sale.

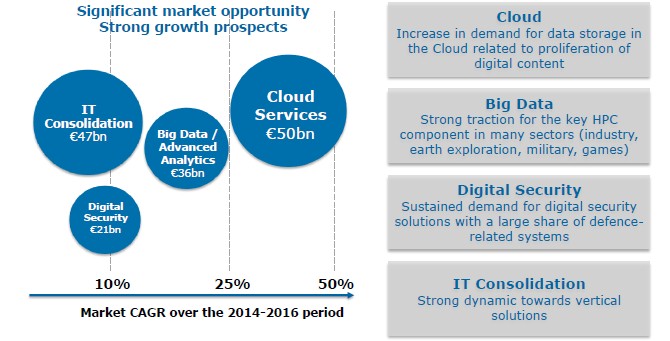

The cybersecurity angle is something that the Atos-Bull combination will play up, and so is cloud computing and what Atos is calling IT consolidation. Each company has over 1,000 engineers dedicated to IT security in one form or the other, and the combination of the two cybersecurity units generated €290 million in sales in 2013. This business is also growing much faster than the IT industry at large.

Add it all up, and Atos and Bull together accounted for €9.9 billion in revenues in 2013, with €4.7 billion coming from managed services (including outsourcing) and another €3.3 billion coming from system integration and consulting. The Worldline online payment service from Atos kicked in another €1.1 billion in revenues, and big data and security (which Atos will collapse into one practice because you can't have one without the other) generated €490 million.

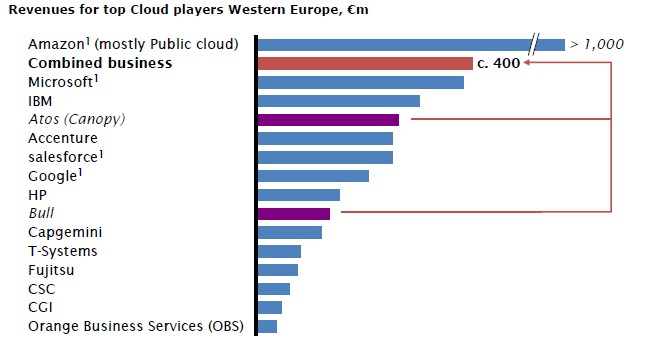

That leaves cloud services, something that both companies have been trying to build up in the past three years, according to Breton. Bull's cloud services business generated €112 million last year and Atos brought in €280 million, for $392 million. This cloud is also growing in the double digits, Breton said, and when you take infrastructure and platform cloud services and roll in software, encryption, identification, and access management services, cloud revenues are around €450 million. But just taking into account the raw cloud services, here is how Atos sees it stacking up in Europe:

Amazon Web Services is predominantly involved in selling public cloud capacity, and is estimated to have more than €1 billion in such sales in Western Europe, according to statistics that Atos gathered up from IDC, TBR, and Synergy Research Group in the chart above. Here's the fun bit. The Bull cloud business plus the Canopy cloud business from Atos together came close to €400 million last year, and while it was mostly for private cloud construction, it is still cloud business and it makes the combined Atos-Bull the number two cloud player in Europe, just jumping ahead of Microsoft and IBM.

Atos says that it has a few ways of pushing up sales and lowering costs with the Bull acquisition. Like IBM's own Power Systems business, the Escala AIX server business from Bull, which includes rebadged Power-based servers from Big Blue with, has been declining over the past several years. Atos says it can mitigate that decline by shifting the procurement of systems for its Atos services clients and for its Canopy cloud from IBM to Bull. (Presumably this will all be for X86 servers, but Atos could be acquiring some Power iron, too.) The company also wants to combine the vertical knowledge of the Atos services business with the scale-out computing capabilities of the Bull business, with a particular focus on the research and development activities of manufacturers.

By eliminating some back office and real estate costs and scaling up purchasing power, Atos thinks it can cut about €80 million in costs over the next two years through the combined companies. Crescendo Industries and Pothar Investments, which together own 24.2 percent of Bull's outstanding shares, have approved the acquisition of Bull by Atos.

Given the indigenous nature of high performance computing and the localized IT needs of governments and some large enterprises, it will be interesting to see if any of the other large IT services companies that do not already have their own systems businesses will be tempted to replicate a similar pairing. This deal for Bull is attractive to Atos for a number of different reasons, but its portfolio of 1,900 patents is important and so is the fact that Atos has pretty balanced sales across the major countries in Europe and across various industry sectors. The combined companies generated 22 percent of sales in 2013 in France, 19 percent in Germany, 17 percent in the United Kingdom and Ireland, and 15 percent in the Benelux and Nordic regions. The company's percent of sales in France were enhanced a bit, but not in a way that makes Atos lopsided.

It is interesting to contemplate what a services giant might do with Cray or SGI. With a market capitalization of $1.14 billion as this story goes to press, Cray has been able to grow sales and net income for the past several years even if you exclude the $140 million it got in 2012 when it sold the "Gemini" and "Aries" interconnect businesses to Intel. Cray has stabilized even as government funding from the Defense Advanced Research Projects Agency for HPC systems was cut back, leaving the US Department of Energy to champion the development of large-scale clusters. Cray weathered the Great Recession under the stewardship of CEO Peter Ungaro and pushed out into storage and repositioned its machines to take on enterprise-class analytics jobs. In 2013, it had $525.7 million in revenues and brought $32.2 million to the bottom line.

SGI also brought in new leadership when it tapped Jorge Titinger to be CEO in early 2012, and has similarly been focused on bringing its shared-memory system and clustering technologies, originally aimed mostly at supercomputing centers, into the enterprise datacenter. SGI had $767.2 million in revenues in 2013, and has reduced its losses significantly as it deals with a cutback in Federal government spending in certain areas of its business. Part of SGI's recovery has been to shift away from the commodity cloud servers and storage space, where it is very tough to make money (unlike in days gone by), and towards the big data and analytics spaces, where the need for shared memory systems is only now becoming apparent to enterprises that are habituated to only deploying clusters. With a market capitalization of $314.1 million and a core business – including traditional HPC, big data systems, storage, and services but excluding legacy cloud and low-margin deals from prior periods – that is growing sequentially at a decent clip, SGI might be an attractive acquisition as well.

SGI and Cray, of course, are focused on partnering with software and services companies to provide exactly the same kind of integrated stacks for analytics, simulation, and other workloads directly to customers as Atos and Bull are talking about once the acquisition is done. No one is suggesting that either Cray or SGI needs to be acquired. But the synergies might make sense, particularly given the deep experience that these two companies have, if the right deal came along.