Transitions, Competition Curb Datacenter Spending Growth

The prognosticators at Gartner have gazed into their crystal balls and now think that spending on servers, switching, and storage in the datacenter is going to be a bit slower than expected this year, and also say that they think spending on IT services will not be as robust as they had hoped. Spending on devices, particularly for smartphones and tablets, is also expected to stall.

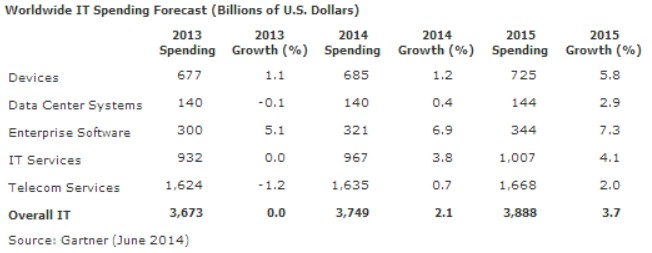

The story is much the same across the different sectors of the IT space, and it is one that we have seen time and time again over the decades. New kinds of devices, both in the datacenter and in our hands and on our laps or desktops, are coming in at lower price points and driving down overall revenues. That said, Gartner is projecting that the world will consume $3.75 trillion in hardware, software, and services in 2014, up 2.1 percent from last year. The most recent forecast by Gartner had pegged overall IT revenue growth of 3.2 percent for 2014, so this is a pretty substantial change.

The company is projecting that global IT spending will grow by 3.7 percent in 2015 to $3.89 billion. Of course, absent any obvious dire economic news, projections are always rosier in in the near-term and long-term when it comes to IT spending, so you always have to take these forecasts with a grain of salt. The important thing is that the global IT budget is still outpacing the aggregate growth in the global economy, but much of this growth is in areas that are outside of the datacenter but which nonetheless impact datacenters because, ultimately, any device talks to many datacenters as it is used.

This year, Gartner now reckons that spending on datacenter hardware will only rise by a mere four-tenths of a percent, essentially flat at $140 billion compared to 2013. Cloud-based storage and a glut in the NAS and SAN markets are putting downward pressure on sales of external storage arrays. On the systems front, spending on hyperscale servers is driving up units, and as EnterpriseTech has pointed out before, these minimalist machines tend to drive down revenues because they have none of the extra bells and whistles that are typically (and unnecessarily) part of a general purpose enterprise server. Redundancy and resiliency features are not required for distributed application, middleware, or database programs. Among consumers, who are the ones using the applications that are by and large deployed on these hyperscale systems, there is a similar shift to what Gartner calls “utility tablets,” which is similarly putting a damper on revenues on for devices. Even still, as you can see from the table above, the market for devices is nearly five times as large as the datacenter market, and it is still growing a lot faster. Companies are trying to wring more efficiencies out of their datacenters and are curbing spending as they do so, and it is probably not reasonable to expect that to change any time soon.

It may, in fact, be unreasonable to expect any increase in spending for datacenter systems going forward, even if there are tectonic shifts underway in the server, storage, and networking markets. The level surface of this datacenter sea does not tell the story of the churning that is going on underneath the surface in every part of the market.

“Price pressure based on increased competition, lack of product differentiation and the increased availability of viable alternative solutions has had a dampening effect on the short term IT spending outlook,” explained Richard Gordon, managing vice president at Gartner, in a statement going over the numbers. “However, 2015 through 2018 will see a return to ‘normal’ spending growth levels as pricing and purchasing styles reach a new equilibrium. IT is entering its third phase of development, moving from a focus on technology and processes in the past to a focus in the future on new business models enabled by digitalization.”

Enterprise software sales are expected to keep humming along, and Gartner now thinks that companies will spend slightly more this year on infrastructure software – operating systems, middleware, databases, application frameworks, and various management programs – and slightly less on application software. Database software, both unstructured and structured, is projected to be especially strong this year. Both infrastructure and application software sales are being impacted by the shift to cloud-based services, whether this is in regards to PC applications that end users have shifted to the Web or services that would normally have been run inside of a private datacenter that are now rented on a monthly basis from a cloud provider.

IT services is expected to uptick a bit in 2014, rising 3.8 percent to $967 billion, but outsourcing revenues are down thanks to a price war for cloud storage and the cannibalization of various datacenter outsourcing services by cloud providers. System integration and implementation services spending is also crimped somewhat as companies focus on smaller projects and IT service providers look at the margins for every deal and walk away from deals that do not make economic sense to them. (This is a healthy attitude and nothing to complain about.)

Gartner includes voice and data services as part of its overall IT spending pie, and one could argue one way or the other whether or not to include it since the telecom portion dominates the global IT bill each year. Telecom services spending shrank by 1.2 percent last year, but is forecast to grow by seven-tenths of a point to $1.64 trillion in 2014 and to grow by another 2 percent to $1.67 trillion in 2015.

If you just look at enterprise software and datacenter systems, what we might consider the core IT market, then revenues will grow by 4.8 percent to $461 billion this year, and by 5.9 percent to $488 billion in 2015. That is still considerably more growth than global gross domestic product. Most people would obviously prefer growth rates for core IT spending and for GDP to be twice as high, a return to the heyday before the Great Recession. But given all of the changes going on in IT and in the global economy, that seems like a lot to wish for.